StudentSpeak – The ISBF Student Blog

How are Interest Rates used to Control Exchange Rate Volatility?

Posted on October 17, 2022 by By Atharva Kulkarni, Harsh Barot, Kritika Soni and Zunaid Rafique | Student Speak

When we talk about the real world macroeconomy, we mostly come across the talk about income, inflation, interest rate, exchange rate, etc. One of the most interesting aspects is to look at the real-world scenarios through the lens of macroeconomic theories and models. This article tries to look at a very intriguing aspect of the real-world economy, which is not restricted to just a few nations, but the world as a whole.

The article begins by looking at the theoretical aspect of how the interest rate as a policy tool is used to control inflation and the exchange rate volatility that arises amongst different countries. Then we try to justify this approach by taking the examples of four countries with different economic conditions. India is taken as a representative of developing nations, while UK represents developed nations. We will look at the exchange rate of these countries with the US$. We include Japan as a representative of currencies against which the INR was appreciating. Turkey is included in the analysis as it’s the only country where the policymakers are following an expansionary monetary policy despite the situation of hyperinflation. So by taking the Indian Rupee, the UK pound, the Japanese Yen and the Turkish Lira, we first look at how the broad money in circulation in these countries has increased over the years, and then look at how the interest rates, inflation and exchange rate of these currencies with US$ move in line, to understand the economic conditions of those countries and to understand how the changes in interest rates have been used to control the volatility in exchange rates.

Introduction

The world as a whole has been facing inflationary pressures from the past few months, with inflation breaking records in the developing as well as developed nations. Recently, the Fed initiated an aggressive interest rate policy in order to tackle inflation. Since March, the Fed has increased the interest rate by 300 basis points (3%), its highest hike since 2006. Similarly, the Bank of England and the Reserve Bank of India have also increased the interest rates to tackle the inflation.

High Inflation across the world is a result of ongoing Russian-Ukrainian war followed by sanctions on Russia which has hiked the prices for crude oil leading to negative supply shock, increasing cost for firms and thus, the prices. Along with the supply constraints, there has been demand driven inflation as a result of the subsiding effect of pandemic since governments infused fiscal stimulus in form of relief packages which drove the demand upward but the increase in demand was not successfully met by the supply of goods and services. The central banks across the world are now intervening and increasing the interest rate to absorb excess liquidity in the market and bring inflation into moderation.

Money supply is a tool to control exchange rate volatility as well. An empirical study conducted in Pakistan found that money supply has an inverse relationship with exchange rate (Ali et al., 2015). This is true as when interest rates are increased (as a contractionary monetary policy), the returns in that certain country are relatively higher compared to the other countries. This attracts foreign capital as investment in that country as lenders become willing to invest in the country. This increases demand for the country’s currency and hence leads to the appreciation of the currency, and relative depreciation of the other currencies.

Interest rates can be used to control inflation as well since inflation can adversely affect exchange rates. The rise in interest rate increases the cost of borrowing causing a reduction in business investments and consumptions which affects aggregate output in the economy, thus leading to rise in unemployment. When there is an increase in unemployment it affects the bargaining power of workers as it becomes difficult to find work, which results in more people being available to work at lower wages. This in return reduces the cost for firms and price levels are reduced. Persistent fall in price level across different sectors helps in bringing inflation in moderation.

Money supply and exchange rate volatility in global context: Empirical evidence

Since March 2022, a fury of Central Banks around the world are raising interest rates in order to combat the ever-growing inflation. There are various researches which have looked at how interest rates may minimize exchange rate volatility indirectly through inflation. For instance, Asari et al. (2011) found that interest rate can be efficient in containing exchange rate volatility in a study conducted in Malaysia. In another study by Khin et al. (2017), they stated that there is a significant short-term relationship between exchange rate volatility and money supply.

Looking at the current conditions of the economies, for instance, we know that as a result of the increase in interest rate by the US Fed, there has been a series of effects on the Indian economy. When the interest rate in the US increased, it made the US financial assets more attractive than the domestic financial assets, which resulted in an increase of demand for US bonds and thus Dollars, depreciating the domestic currency (INR). For foreign portfolio investors (FPIs), the rupee’s decline affects the returns. FPIs lost their equity assets totaling US$ 4.46 billion in February 2022, and US$ 4.71 billion more were sold under these challenging circumstances and market instability. The forex market’s supply and demand for foreign currency both have an impact on the exchange rate at any given moment. As is the case right now, when outflows of resources denominated in US dollars outpace inflows, the dollar rises while the INR depreciates.

Due to the depreciation of the currency, there was an increase in the import bills which increased the cost of importing raw materials and thus increasing the cost of firms, which led to increase in prices and imported inflation. The predictions of the Fed’s aggressive monetary tightening plans and rising energy costs helped the dollar gain ground against the INR despite ongoing inflows of foreign funds. India imports more than 80% of its oil needs, hence oil prices have a considerable impact on both the country’s trade balance and current account deficit.

The depreciation of the INR against the US$ also led to lack of funds available for Indian firms as a result of attractive interest rates in the US leading to portfolio outflow. It also increases the cost of borrowing for the government which increases the debt to GDP ratio indicating a bad health of the economy.

Now, we look at the money supply, inflation, interest rates, and exchange rate relationships of these four countries.

a.) The Indian Rupee (INR)

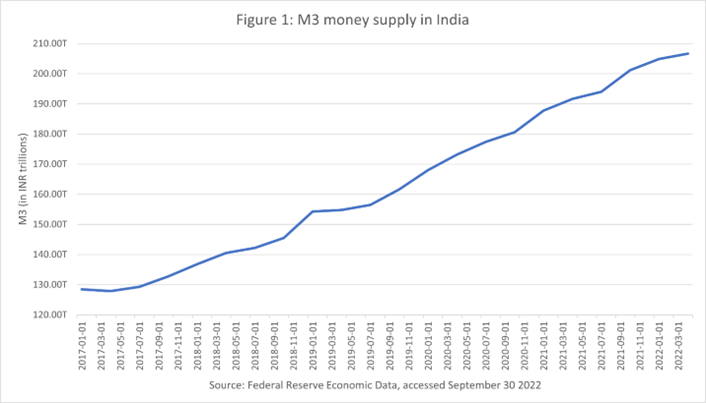

One of the best examples to look for exchange rate volatility right now is the INR against the US Dollar. In India, the M3 money supply (broad money) has been steadily increasing from 160 trillion rupees since the start of 2020 (figure 1).

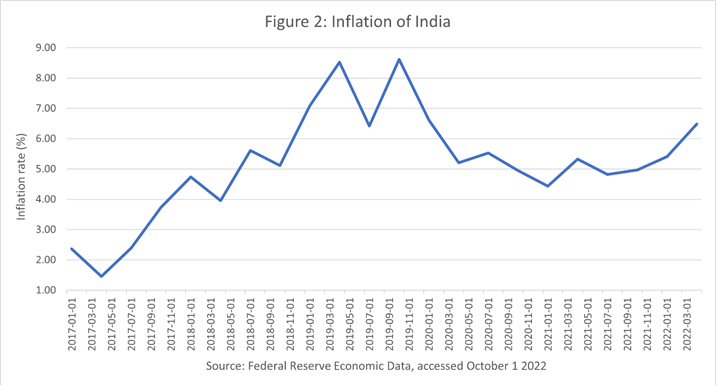

This led to rising inflation in the post-pandemic period as the economy opened and the demand revived, while there were still supply chain disruptions. This inflation was further aggravated by the Russia-Ukraine crisis (figure 2).

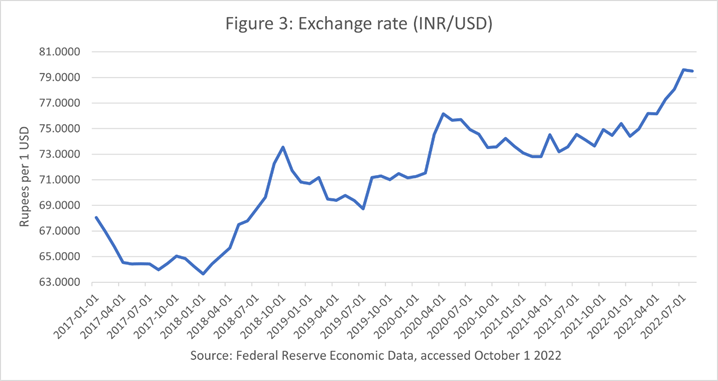

Now, as Fed started hiking the interest rates to tackle inflation in the US, the Rupee started to depreciate from April 2022 and broke the ₹77 mark in mid-May 2022 as seen below (figure 3).

The INR has been depreciating since then, breaking the 82 rupees mark just a couple of days ago. An empirical study conducted by Nath et al. (2022) found that exchange rate volatility has decreased over time, especially in the case of the Rupee. One of the main reasons for this is the accumulation of forex reserves by the RBI. The increase in forex reserves has been significant since 2014 and has been vastly increased since 2020.

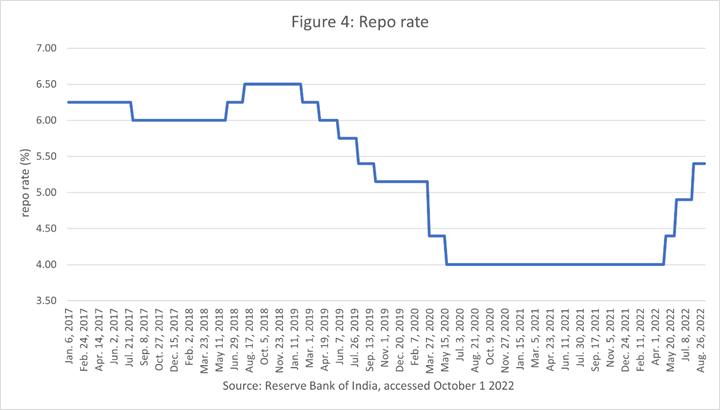

Apart from the use of forex reserves, which can only be used temporarily to prevent exchange rate volatility, as the theory suggests, RBI used interest rate to control this volatility. The RBI has been increasing the repo rate since mid-April 2022 (figure 4).

Regardless of the increases in the repo rate by the RBI till now, the rupee has kept on depreciating. It also does not help the fact that the Fed has been incredibly aggressive in its rate hikes. This has strengthened the dollar even more resulting in further depreciation of the rupee. Just at the end of September 2022, RBI has hiked the repo rate to 5.9%.

If the Fed is ever more aggressive in its upcoming hikes (which is highly anticipated), then there will be further pressure on the rupee as the exchange rate is heavily affected by the Fed’s decisions. The weakening of the rupee will adversely affect inflation as much of the inflation for India is imported inflation, which has been steadily rising as it is.

b.) British Pound

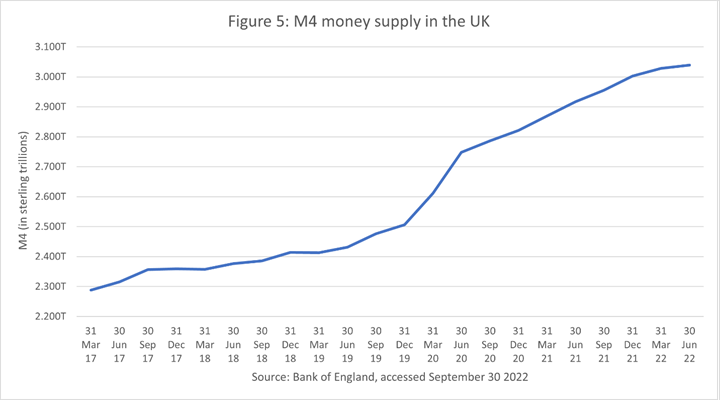

Looking at the British Pound, the M4 money supply (broad money) of the United Kingdom greatly increased from February 2020 and kept the steady increase till July 2020. This is to be expected as the COVID-19 pandemic started to pick up and the policy of expansionary monetary policy was used to stimulate growth (figure 5).

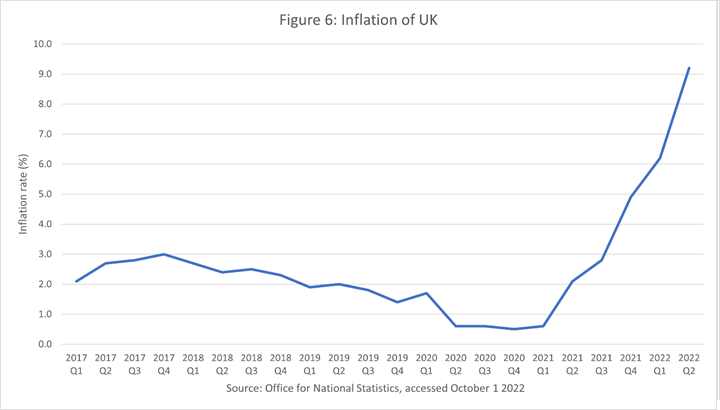

Inflation started to pick up in February 2021 and has kept on increasing as the economies began to open and demand revived from the pandemic, while the supply did not.

As the Fed raised interest rates to tackle inflation, the British pound started losing ground against the dollar since January 2022. It has depreciated to £0.92 and is very likely to breach the £1 mark (figure 7).

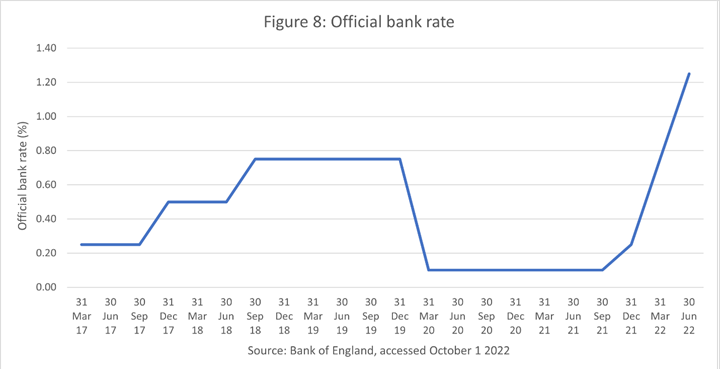

The Bank of England (BOE) has been just as aggressive as the Fed in increasing its official bank rate to tackle the exchange rate volatility. The BOE has raised its official bank rate by 2.15% since December 2021 (figure 8).

Even with continued increase in bank rate, the pound has depreciated even further reaching its lowest value since 1985 as the current hike and the anticipated hike by the Fed has incentivized investors all over the world to pull out money from other countries and invest it in the US, leading to outflow of funds from other countries, and inflow of funds in the US. This has further led to appreciation of US$ and depreciation of other currencies, here, the British pound.

c.) Japanese Yen

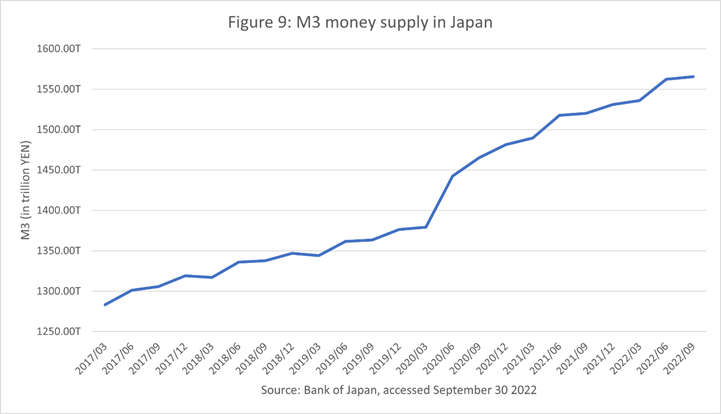

Akin to the money supply changes in all other countries, the M3 money supply of Japan has been on a rise (figure 9).

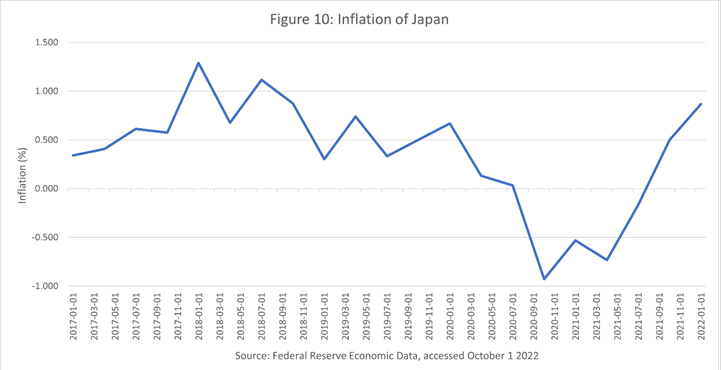

And, just like other countries, there has been a resultant rise in inflation.

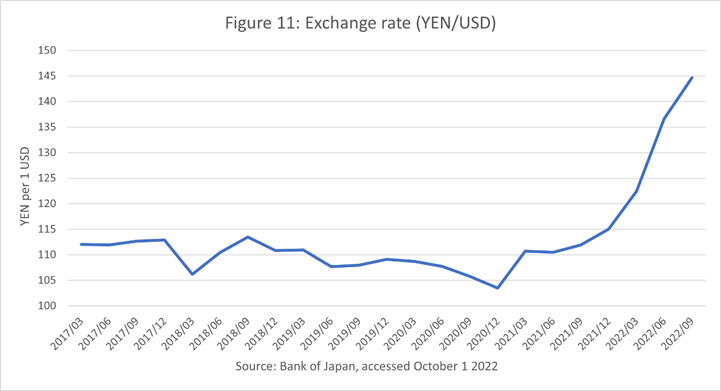

This, as we can see in figure 11, that just within 2022, the currency has depreciated by close to 30¥.

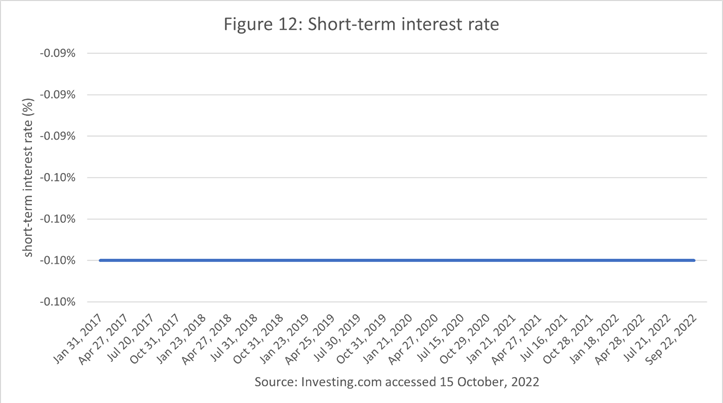

To tackle the inflation, while the central banks across the world raise their interest rate, the Bank of Japan (BOJ) has taken an unconventional approach as compared to most of the central banks. The short-term interest rate has been kept unchanged at -0.1% which has remained the same since 2016. The BOJ has done this to facilitate demand-driven inflation which it has said is missing from the inflation Japan is facing and that it is mainly imported inflation which is driving up consumer prices.

As the BOJ has decided to keep the interest rates unchanged, the Government of Japan had to intervene to save the depreciating Yen, a move which has not been seen since 1998. With rising cost of imports and inflation, it will start to hurt the production costs of domestic manufacturers resulting in lower imports.

d.) Turkish Lira

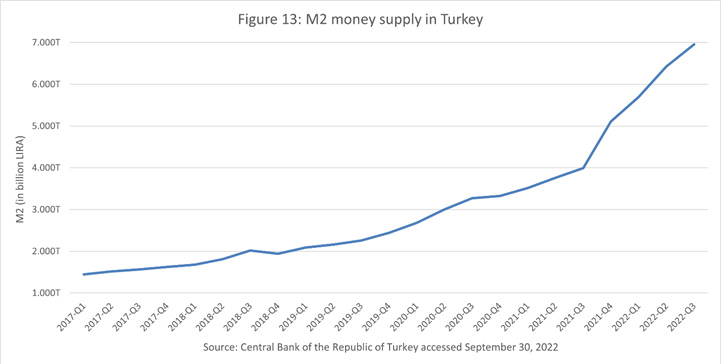

The M2 money supply in Turkey significantly increased from January 2020 to October 2020 and then again from October 2021 till now, like other nations of the world (figure 13).

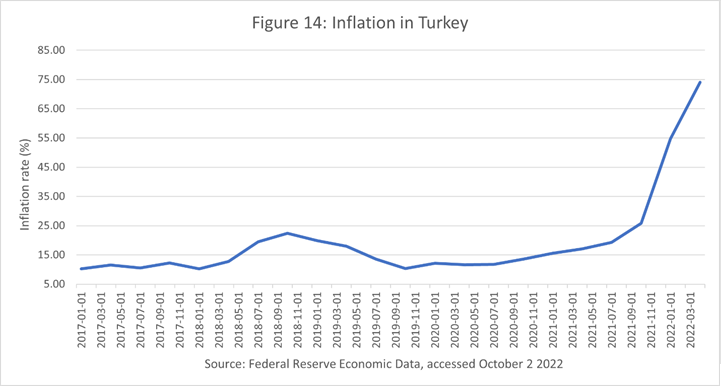

Due to the reasons stated for all other countries, it led to inflation in the Turkish economy post the pandemic.

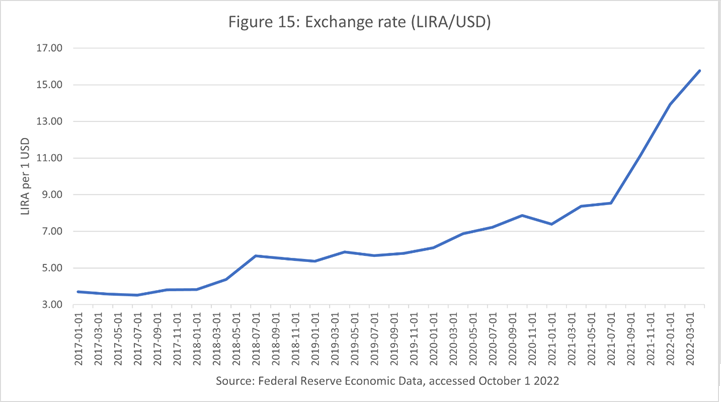

This led to the depreciation of Turkish Lira, which is the similar case as what happened with all other currencies.

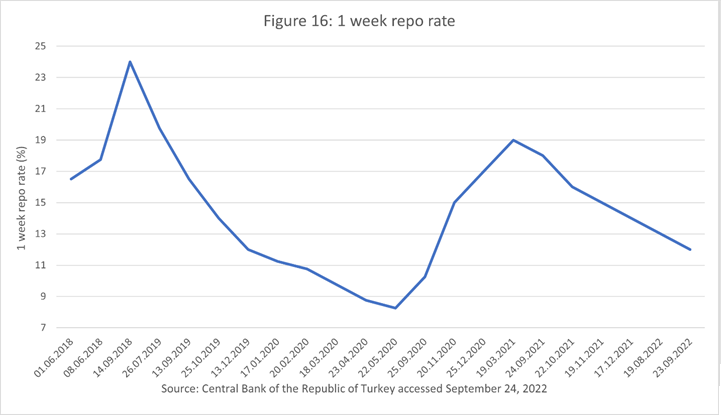

Now, the central bank of Turkey should have increased the interest rate to tackle the inflation and exchange rate volatility, but the Central Bank of Turkey is doing the opposite of the majority of the Central Banks. It has cut interest rates from as high as 19% in March 2021 to just 12% in September 2022, as the government believes that high inflation is the outcome of high interest rates. The government is cutting interest rate to stimulate domestic investment and support export-oriented sectors.

This comes at a time when the Turkish economy is experiencing 80% inflation and a debt crisis. This has had a major impact on the Turkish Lira which has depreciated increasingly since September 2021. Inflation has reached a staggering 80% and the Central Bank of Turkey has kept cutting interest rates. With such a high inflation rate and major depreciation of the Lira, imports are bound to become significantly more expensive.

Conclusion

Through the empirical analysis of these four currencies, we can conclude that most of the central banks across the world use interest rates to tackle inflation and exchange rate volatility. Although the effectiveness of interest rate as a tool depends on the relative interest rates of various countries. For instance, as seen in the above cases, most of the central banks raise interest rates but there is still an outflow of US$ because the hike in interest rate and the anticipated hike by the Fed are more, relative to the hikes of other major central banks. Thus, the relationship between these variables does exist, and no doubt the policymakers can make use of it to achieve its objectives, but it’s effectiveness will also depend on other factors, which might be uncontrollable.

Written by:

Atharva Kulkarni: Atharva Kulkarni is an Economics student at ISBF UOL and an avid enthusiast of economics.

Harsh Barot: Harsh Barot is currently completing his final year in Economics & Finance from ISBF UoL. And was also the former Vice-President of the student council in the institute.

Kritika Soni: Kritika Soni is a Economics student at ISBF UOL and an economics enthusiast.

Zunaid Rafique: Zunaid Rafique is a final year Economics and Management undergraduate at ISBF UoL and was the VP of investment cell. He is a finance enthusiast with relevant work experiences and volunteers for poverty elevation in India.

Mentored by:

Payal Sharma

Assistant Professor (Economics), ISBF